matt haugen

matt haugen

Why does Twin Cities Habitat have a home listed on the MLS?

We continue to process the pain and hope of our nation’s uprising for racial justice amid a global health crisis. You can see our recent statements...

We continue to process the pain and hope of our nation’s uprising for racial justice amid a global health crisis. You can see our recent statements on the uprising here, our COVID-19 web page here, and our Race & Housing resource center here. Expanding homeownership is a key component of racial equity and health, so our mission has never been more important—and we’ll continue to share the stories of Habitat’s work.

Twin Cities Habitat for Humanity has a core value of Equity and Inclusion which states: “We promote racial equity and strive to increase diversity, inclusion, and cultural competency in all aspects of our organization.” We believe that it’s important to learn from our national and local history of racist housing policies as we build for the future. This blog series explores the past, offers solutions for the future, and highlights ways that you can take action.

For more than a century, homeownership has been the primary way Americans have built wealth and passed it on to future generations. We can’t talk about racial wealth inequalities without talking about homeownership and the tax codes that support it.

While housing policy isn’t explicitly racist today like it was decades ago, systemic racism is still very present. The mortgage interest deduction (MID) is one example. Here’s how it works in a nutshell. If you own a home and have a home loan, at tax time you can take all the interest you paid on that loan during the year and deduct it from the taxable income you received. By lowering your taxable income, it lowers the amount of taxes you need to pay. Essentially, the government subsidizes you to pay your mortgage interest. The bigger the mortgage, the more money you save.

So how is systemic racism involved?

The MID has been around since 1913. Back then only the top 2% of earners in America paid any income tax at all – so this deduction didn’t get a lot of attention at the time. It really took off following World War II when more Americans began buying homes (and paying income taxes). However, during the ensuing decades homeownership opportunities were not equally available and racism was openly practiced via mortgage redlining, racial deed covenants, and access to the benefits of the GI Bill. Each of these deliberately excluded Black people and other groups from becoming homeowners. As home values and incomes rose, the value of the MID (or cost to taxpayers) grew and the money disproportionately went to White households.

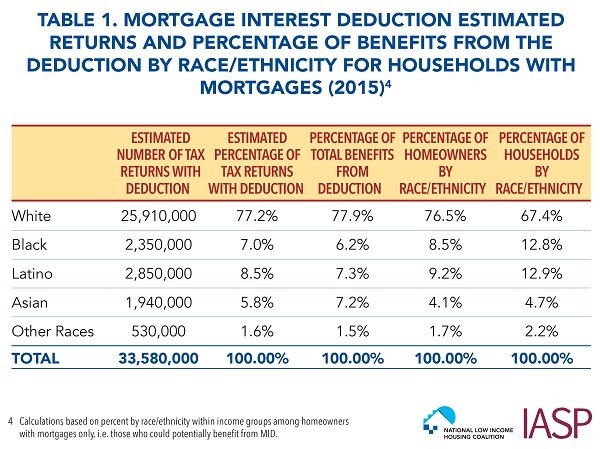

As shown in the chart below, even though White Americans make up 67.4% of households, they reap 77.9% of the benefits of the tax deduction because of their high homeownership rights thanks to decades of preferential treatment. Even Black Americans who do own homes (8.5% of homeowners) receive a smaller percentage (6.2%) of the total benefits from the MID.

Matthew Desmond, the Pulitzer Prize winning author of Evicted, says the MID was key to homeownership increasing inequality in America. Over the years, the MID has become less about helping families become first-time homeowners and more about helping families buy bigger, more expensive homes—or even second homes.

Economists say the MID drives up home prices and you can see why when you consider how much it saves a family based on how big a mortgage they take out. A family with a $250,000 mortgage at 4% interest will pay $180,000 in interest over the 30 years of their loan. That means they’ll be able to deduct $180,000 from their taxable income over those 30 years through the MID. Larger mortgages create larger deductions: a $500,000 mortgage translates into $359,000 in deductions. If a family maxed out the deduction with a $750,000 mortgage, they’d be able to deduct $539,000.

By 2017, the MID had grown into a $70 billion per year subsidy (by far the largest housing subsidy in America). The tax changes passed in 2018 increased the standard deduction and meant fewer families itemized and took the MID. The total cost of the MID is still about $30 billion a year. But the benefits are now even more tilted towards top earners. Before the tax changes, 4% of the benefit went to households with at least $1 million in annual income. Now it's estimated 10% of the benefit goes to this group.

Economists forecast the mortgage interest deduction will grow in the years ahead, especially when the cap on mortgage sizes is raised from $750,000 to $1,000,000 in 2025.

This structure incentives people to borrow more and buy more home. It also increases the likelihood of a default or foreclosure for homeowners who hit major financial setbacks.

Economists don’t like the mortgage interest deduction because it distorts the housing market. A study from 2018 predicted if we eliminated the deduction, we’d see a 5% increase in the homeownership rate, a 4% drop in home prices, and 30% decline in the average mortgage balance.

Replacing the deduction with a credit could do even more to put homeownership within reach for those who have historically been denied opportunities. Tax credits directly reduce the amount of taxes you owe, rather than reducing your taxable income, which would benefit lower income earners more than higher income earners. If a tax credit is refundable, it can be an even bigger boost for lower income earners.

Prosperity Now drafted changes that could tilt the benefits of our tax code back toward households in the bottom half of wage earners. One idea is a $1,200 annual tax credit for all homeowners in place of the mortgage interest deduction.

Prosperity Now drafted changes that could tilt the benefits of our tax code back toward households in the bottom half of wage earners. One idea is a $1,200 annual tax credit for all homeowners in place of the mortgage interest deduction.

Because of the scale of the problem, we cannot build our way out of all the racial inequalities in housing. In the Twin Cities, three out of four white families own homes compared to one in four black families.

This gap is the culmination of historic racism that is now perpetuated in part by a tax system designed to maintain the status quo. Please join Twin Cities Habitat and others in advocacy efforts to rethink how we can promote equity and shared prosperity via our housing policies.

Your gift unlocks bright futures! Donate now to create, preserve, and promote affordable homeownership in the Twin Cities.

We continue to process the pain and hope of our nation’s uprising for racial justice amid a global health crisis. You can see our recent statements...

We continue to process the pain and hope of our nation’s uprising for racial justice amid a global health crisis. You can see ourrecent statements...

.png)

We continue to process the pain and hope of our nation’s uprising for racial justice amid a global health crisis. You can see ourrecent statements...