Greta Gaetz

Greta Gaetz

Six things you might not know about affordable housing

You might hear the term “affordable housing” used often, whether in the news or by someone you know. Sometimes misconceptions around affordable...

Written by Greta Gaetz and Kaitlyn Dormer.

Twin Cities Habitat for Humanity has a core value of Equity and Inclusion which states: “We promote racial equity and strive to increase diversity, inclusion, and cultural competency in all aspects of our organization.” We believe that it’s important to learn from our national and local history of racist housing policies as we build for the future. This blog series explores the past, offers solutions for the future, and highlights ways that you can take action.

If you’ve kept up with the Race and Housing Series, you’ve read about how racial covenants and bank redlining led to the Twin Cities’ segregated neighborhoods and persistent disparities. You’ve also heard largely untold stories of resistance—moments in history when residents took action against racist policies to push our communities forward.

Decades of active resistance pushed our country toward the passing of the Fair Housing Act in 1968. This historic legislation expressly forbids racial discrimination in housing and began the slow process of desegregation which continues today.

But in the wake of the Fair Housing Act, banks still managed to avoid lending to would-be borrowers living in low-income neighborhoods. Racist redlining persisted.

Then in 1977, the federal Community Reinvestment Act (CRA) was enacted to reverse the effects of redlining and encourage banks to meet the credit needs of the low-income and moderate-income neighborhoods where they operate.

Twin Cities Habitat’s Chief Strategy Officer, Robyn Bipes-Timm, simplifies the CRA in this way: “Wherever a bank has a brick and mortar location that takes deposits or holds checking and savings accounts for residents, that bank must also reinvest in those people by making loans available.”

Three federal regulators—the Office of the Comptroller of the Currency (OCC), the Federal Deposit Insurance Corporation (FDIC), and the Board of Governors of the Federal Reserve System—share oversight of the banks’ compliance with the CRA. Banks are rated on a four-point scale, and bad ratings can impact borrowing ability, price of capital, and other regulatory consequences.

Put simply, regulators assess if banks are:

The CRA has played a key role in encouraging banks to meet the credit needs of low-income and moderate-income communities, and it has reduced the effects of racist redlining in cities across the country.

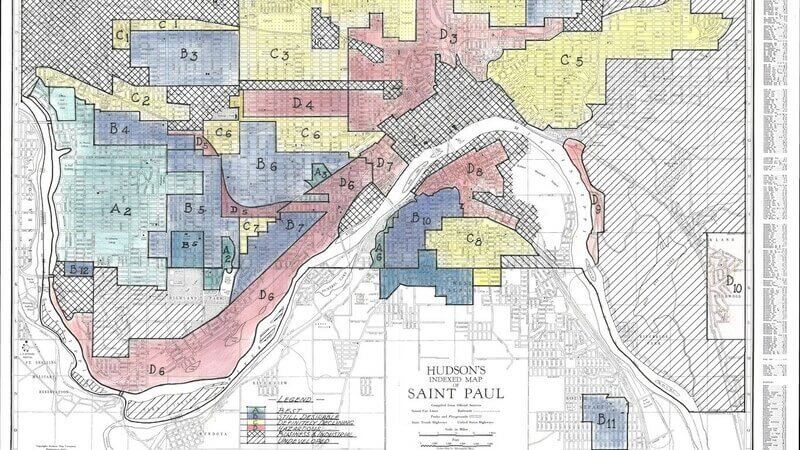

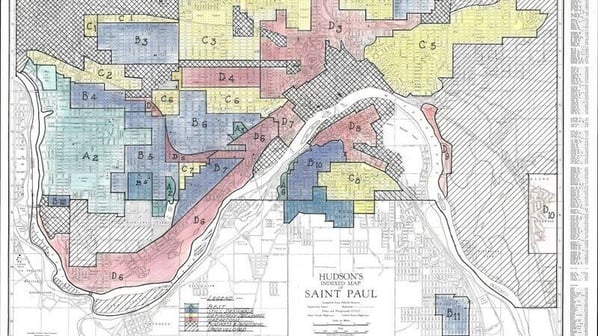

A map of redlining in Saint Paul.

Working hand in hand with local banks is vitally important to furthering the mission of Twin Cities Habitat for Humanity, and these relationships are meaningful to our banking partners as well. For example, our strong partnership with Bremer Bank created the Home Loan Impact Fund, through which Bremer has agreed to purchase 500 below-market Habitat mortgages over four years. The Home Loan Impact Fund will more than double the number of families that can partner with Twin Cities Habitat on affordable homeownership.

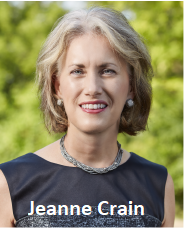

“Community partnerships have been a defining characteristic of Bremer Bank since our founding,” says Jeanne Crain, President and CEO of Bremer Financial Corporation. “Bremer is built on the belief that together, banking and commerce can help communities thrive.”

“Community partnerships have been a defining characteristic of Bremer Bank since our founding,” says Jeanne Crain, President and CEO of Bremer Financial Corporation. “Bremer is built on the belief that together, banking and commerce can help communities thrive.”

Many of our banking partnerships are incentivized by the CRA. Partnering with Twin Cities Habitat allows banks like Bremer to make a meaningful investment in the community and demonstrate that commitment through the CRA, all while greatly extending Habitat’s ability to provide affordable mortgages to lower-income families.

“The Community Reinvestment Act provides an opportunity for all banks to live out the value of community service,” says Crain. “One of the most impactful ways Bremer has recently lived out this value is through our partnership with Twin Cities Habitat for Humanity. We are proud of the Home Loan Impact Fund, the people it has helped, and its legacy throughout the country.”

Right now, there are several proposed changes to the CRA which could have significant impacts on lending for affordable homeownership, lending to low-income and minority communities, and private investment in affordable homes overall. Habitat for Humanity affiliates across the country believe that the CRA must remain consistent to meet the credit and banking needs of lower-income and moderate-income people.

Twin Cities Habitat for Humanity also believes it is important that banks have incentives to invest in affordable homeownership. Reducing these incentives strays from the original purpose of the CRA and threatens to draw lending capital away from the lower-income homebuyers who we partner with. Instead, we support a continued strong implementation of the CRA that provides a meaningful measurement of investment in lower-income communities.

Twin Cities Habitat submitted comments to the OCC and FDIC on April 7 urging them to revise their proposal to ensure that any changes to the CRA will not reduce the availability of direct lending, investments, and financial services for lower-income and moderate-income homebuyers and communities.

To stay up-to-date on actions you can take to support affordable housing policies, sign up for our advocacy action alerts.

Sources:

Your gift unlocks bright futures! Donate now to create, preserve, and promote affordable homeownership in the Twin Cities.

You might hear the term “affordable housing” used often, whether in the news or by someone you know. Sometimes misconceptions around affordable...

Racial equity and anti-racism are embedded in our mission, vision, and values. We strive to learn from our national and local history of racist...

We continue to process the pain and hope of our nation’s uprising for racial justice amid a global health crisis. You can see ourrecent statements...