Regina Eckes

Regina Eckes

The History and Current State of Minnesota's Homeownership Gap

"Homeownership rates remain at historic lows, falling to 63% for the eighth consecutive year of decline and contributing to crowding and rising...

A January 2024 article by NPR reported on a study that found housing is now unaffordable for a record half of all U.S. renters. When we focus on Minnesota, the stats are even more staggering. We’ve come a long way in correcting the previous wrongs of racially based housing policies and lending practices like redlining and racial covenants, and the Twin Cities Black population has increased. But the homeownership rate is lower than ever. How can that be?

We’ve exposed the truth about redlining, displacement of populations, and the destruction of thriving Black communities throughout our history. We outline many of these in our Race & Housing blog series. Great strides have been made to correct these past errors, but reports from 2005 and onward show that the homeownership rate for Black Minnesotans actually continues to fall, and the homeownership gap between white and Black households grows wider.

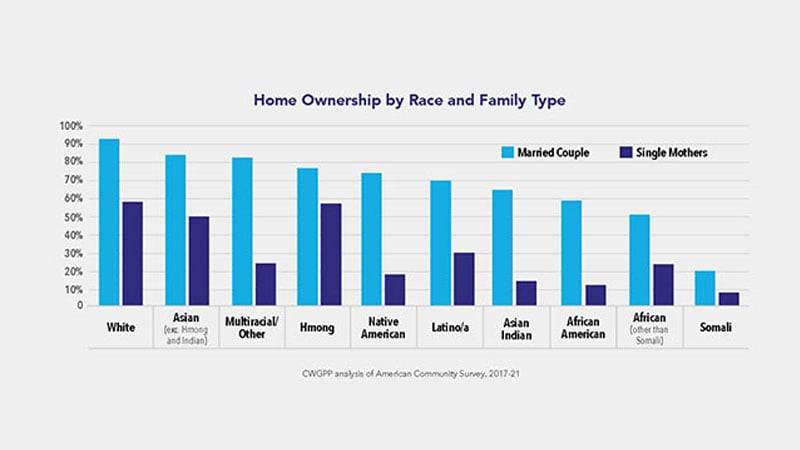

We looked at data from the Prosperity Now Scorecard, which is a comprehensive resource featuring data on family financial health, racial economic inequality, and policy. Their 2015-2020 study shows 77.5% of white households own their home in Minnesota compared to just 30.5% of Black households, and the number is even lower in the metro area. Among white, Black, Native, Asian, multiracial, and Hispanic/Latinx groups, Black homeownership was the lowest. The Scorecard also found that 45.5% of white renting households in Minnesota are cost-burdened, compared to 57.4% of Black renting households.

Prosperity Now Scorecard

Prosperity Now Scorecard

A MinnPost article from July 2022 provides several explanations for why Minnesota’s Black homeownership rate keeps falling. One reason is continued segregation. It may not be as obvious as it was in the Jim Crow era, but segregation is still present in nuanced ways. In the early 2000s, Black communities were quietly sequestered to certain parts of the Twin Cities, even certain school districts. As the MinnPost article states, “As more Black people began living in closer and closer quarters in Minneapolis, they present neat, concentrated pockets for unscrupulous bankers and real estate firms to swoop in with bad financial products like subprime loans, take the home back from the Black family in foreclosure, stripping them of their wealth.”

A MinnPost article from July 2022 provides several explanations for why Minnesota’s Black homeownership rate keeps falling. One reason is continued segregation. It may not be as obvious as it was in the Jim Crow era, but segregation is still present in nuanced ways. In the early 2000s, Black communities were quietly sequestered to certain parts of the Twin Cities, even certain school districts. As the MinnPost article states, “As more Black people began living in closer and closer quarters in Minneapolis, they present neat, concentrated pockets for unscrupulous bankers and real estate firms to swoop in with bad financial products like subprime loans, take the home back from the Black family in foreclosure, stripping them of their wealth.”

That brings us to 2008. Many BIPOC communities are still reeling from the recession and housing collapse. In the 2021 research report Who Owns the Twin Cities? An Analysis of Racialized Ownership Trends in Hennepin and Ramsey County, many Twin Cities homes that fell into foreclosure around 2008, especially on the north side, were purchased in large quantities by huge corporations and converted into single-family rentals (SFRs), which brought in higher-income renters. Between 2005 and 2020, the number of SFRs in Ramsey and Hennepin counties grew from 22,000 to more than 48,000 homes. And the result? “The Black homeownership rate fell from about 31 percent in 2000 to 24 percent in 2010 and to just 21 percent in 2018.”

The report also shows that between 2000 and 2010, the Twin Cities saw tremendous growth in the African immigrant population. But the homeownership data correlates with neighborhood changes, too. Investor landlords targeted SFR investments in low-income and BIPOC neighborhoods.

The report also shows that between 2000 and 2010, the Twin Cities saw tremendous growth in the African immigrant population. But the homeownership data correlates with neighborhood changes, too. Investor landlords targeted SFR investments in low-income and BIPOC neighborhoods.

Underwriting is also a huge deal when it comes to potential homeowners securing loans. Often, underwriting is the final decision-maker when approving a loan, but for decades, underwriting has been intentionally designed to serve white families with higher incomes.

We can’t talk about the homeownership gap without commenting on the wage gap between white and Black households in Minnesota. The state’s median household income is $80,862 for white households and $47,739 for Black households—staggering. And, between 2015-2020, median rents have risen by 21% while the median annual income for renters has risen just 2%.

Prosperity Now Scorecard

Prosperity Now Scorecard

The homeownership disparity feeds the income disparity and vice versa. Homeowners are able to pass their home to their children or use it as leverage to secure other loans for financing their kids’ education—this is how generational wealth is built. When Black families are unable to own homes, they’re missing out on wealth to pass on to their children and the cycle continues.

Closing the racial homeownership gap takes a lot of work from every corner of our communities. For Twin Cities Habitat specifically, public funding is often the first source for a Habitat project and leverages a significant return on investment through private support from individual donors, congregations, foundations, and corporations. You can help by joining your fellow Habitat supporters to advocate for housing support at the federal, state, and local levels. Here are two actions you can take right now:

The homeownership gap is daunting, but there's hope when we work together. In 2023, after years of advocacy from Habitat supporters and others, the Minnesota legislature created the First Generation Down Payment Assistance program. This groundbreaking new policy will give first-generation homebuyers the financial boost they need to get into homeownership—folks who don't have that generational wealth from homeownership to draw on. It's a great first step towards helping to close that homeownership gap, and with your help, we can go further together.

Your gift unlocks bright futures! Donate now to create, preserve, and promote affordable homeownership in the Twin Cities.

"Homeownership rates remain at historic lows, falling to 63% for the eighth consecutive year of decline and contributing to crowding and rising...

This guest blog post by Tiffani Daniels is part two of a four-part blog series about our partnership with the Minnesota Business Coalition for Racial...

1 min read

Twin Cities Habitat has a core value of Equity and Inclusion which states: “We promote racial equity and strive to increase diversity, inclusion, and...